Welcome to our comprehensive guide on understanding APIC accounting! If you’ve been struggling to grasp the ins and outs of APIC (Additional Paid-In Capital) accounting, you’ve come to the right place. In this article, we’ll break down the key concepts of APIC accounting in a simple and easy-to-understand manner, helping you navigate through this important aspect of financial reporting with confidence. Whether you’re a seasoned professional or just starting out, this guide will provide you with all the essential information you need to know about APIC accounting.

Overview of APIC Accounting

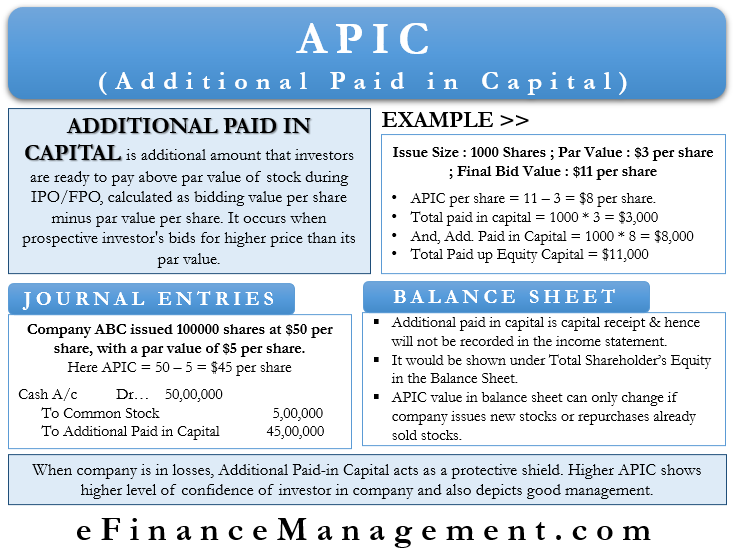

Additional Paid-In Capital (APIC) is a term used in accounting to describe the excess amount of capital that a company receives from investors above the par value of the company’s stock. When a company issues stock, the proceeds above the stated value of the stock are recorded as APIC. This account is listed in the shareholders’ equity section of the balance sheet and is a key indicator of the company’s financial health.

APIC is important because it represents the amount of money that shareholders have contributed to the company beyond the actual value of the stock. This additional capital can be used to fund new projects, expand operations, or pay off debt. It is essentially “extra” money that the company can use to improve its financial position.

When a company issues new shares of stock, the amount received from investors is typically divided between the par value of the stock and APIC. The par value is the nominal value of the stock as determined by the company, while APIC represents the premium paid by investors for the stock. For example, if a company issues 1,000 shares of stock with a par value of $1 per share and sells them for $10 per share, the company would record $1,000 as the par value of the stock and $9,000 as APIC.

APIC can also be affected by other transactions, such as stock-based compensation or acquisitions. Stock-based compensation involves issuing stock options or shares to employees as part of their compensation package. The amount of APIC generated from stock-based compensation is based on the fair value of the stock at the time of issuance. Similarly, when a company acquires another business, the excess amount paid above the fair value of the acquired company’s net assets is recorded as APIC.

One important thing to note about APIC is that it does not represent actual cash that the company has on hand. It is purely an accounting entry that reflects the excess amount of capital contributed by shareholders. However, APIC can be a valuable source of funds for a company, especially when it needs to finance new projects or acquisitions.

In conclusion, APIC accounting is a critical aspect of financial reporting that provides insight into the amount of capital contributed by shareholders above the par value of a company’s stock. It is important for investors and analysts to understand how APIC is calculated and its impact on a company’s financial health. By accurately recording and disclosing APIC, companies can provide a more transparent picture of their financial position and potential for growth.

Importance of APIC in financial reporting

Additional Paid-In Capital (APIC) is a crucial component of financial reporting for companies. APIC represents the excess amount collected from the issuance of stock over its par value. It is a valuable resource for companies as it provides a clear picture of the capital contributed by shareholders that exceeded the nominal value of the shares. APIC plays a significant role in financial reporting and has several important implications for businesses.

One of the key reasons why APIC is important in financial reporting is that it helps in providing a more accurate reflection of a company’s financial position. By including APIC in the financial statements, companies can show the true value of the equity provided by shareholders. This helps in presenting a more comprehensive view of the company’s capital structure and its ability to raise funds through equity financing.

Furthermore, APIC also plays a crucial role in determining a company’s retained earnings. Retained earnings are the cumulative net income that a company retains within the business after paying dividends to shareholders. APIC is used to adjust the initial paid-in capital when calculating retained earnings. This adjustment ensures that the financial statements accurately capture the capital contributed by shareholders that exceeds the par value of the stock.

Moreover, APIC is essential for compliance with accounting standards and regulatory requirements. APIC is reported on the balance sheet as a separate component of shareholder’s equity, ensuring transparency in financial reporting. By including APIC in the financial statements, companies demonstrate adherence to accounting principles and regulatory guidelines, which enhances credibility and transparency for investors and other stakeholders.

Additionally, APIC also provides important information for investors and analysts while evaluating a company’s financial health and performance. The amount of APIC reflects the capital contributed by shareholders in excess of the par value of the stock, giving insights into the equity financing activities of the company. This information can be valuable for investors in assessing the company’s ability to raise capital and its financial stability.

In conclusion, APIC is a critical element in financial reporting that provides valuable insights into a company’s equity financing activities, financial position, and compliance with accounting standards. By including APIC in the financial statements, companies can present a more accurate representation of their capital structure and demonstrate transparency in reporting. Investors and stakeholders rely on APIC to assess a company’s financial health and performance, making it an essential component for companies seeking to attract investment and maintain credibility in the market.

Calculating APIC for stock option compensation

Stock options are a popular form of compensation for employees, allowing them to purchase company stock at a predetermined price. When employees exercise their stock options, the company can recognize additional paid-in capital (APIC) on its financial statements. The calculation of APIC for stock options involves several steps to ensure accurate reporting.

The first step in calculating APIC for stock options is determining the fair value of the options at the grant date. This fair value is typically calculated using an option pricing model, such as the Black-Scholes model. The inputs to the model include the current stock price, the exercise price of the options, the expected volatility of the stock price, the expected term of the options, and the risk-free interest rate. By inputting these variables into the model, companies can determine the fair value of the options granted to employees.

Once the fair value of the options has been determined, the company must calculate the total APIC to be recorded on its financial statements. This total APIC is the difference between the fair value of the options and the total exercise price paid by employees to exercise the options. For example, if the fair value of the options is $10 per share and employees pay $5 per share to exercise their options, then the total APIC would be $5 per share ($10 – $5).

In addition to calculating the total APIC, companies must also determine the timing of recognizing this APIC on their financial statements. APIC for stock options is typically recognized over the vesting period of the options, which is the time period over which employees become entitled to exercise their options. This means that the total APIC is recognized as an expense on the income statement each year equal to the portion of the options that have vested.

It is important for companies to carefully follow accounting standards and guidelines when calculating APIC for stock option compensation to ensure accurate financial reporting. By accurately determining the fair value of the options, calculating the total APIC, and recognizing this APIC over the vesting period, companies can provide transparency and clarity in their financial statements regarding the impact of stock option compensation on their financial performance.

Differences between APIC and common stock

Additional Paid-In Capital (APIC) is a commonly used accounting term that refers to the amount of capital that a company has received from shareholders in excess of the par value of the common stock. On the other hand, common stock represents the amount of capital that a company has raised by issuing shares at a specified value. While both APIC and common stock play a crucial role in the financial structure of a company, they differ in several key ways.

One of the main differences between APIC and common stock lies in their sources. APIC is generated when a company issues shares at a price higher than their par value. This excess amount is considered to be a form of capital that contributes to the company’s total equity. Common stock, on the other hand, represents the original investment made by shareholders when they purchase company shares at their par value.

Another key difference between APIC and common stock is in their accounting treatment. APIC is recorded as a separate line item on the balance sheet, under the stockholders’ equity section. It reflects the amount of capital that a company has received from shareholders in excess of the par value of the common stock. Common stock, on the other hand, is also recorded in the stockholders’ equity section but represents the amount of capital that was raised by issuing shares at a specified value.

Furthermore, APIC and common stock differ in terms of their impact on corporate financial statements. APIC is considered a part of the total equity of a company and can have a significant effect on metrics such as return on equity and debt-to-equity ratios. Common stock, on the other hand, represents the base level of capital that a company has raised through the issuance of shares and may not directly impact these financial ratios.

Moreover, APIC and common stock play different roles in the capital structure of a company. APIC is typically generated through activities such as stock option exercises, stock grants, and other equity-related transactions. It represents the excess capital contributed by shareholders beyond the par value of the common stock and can be used for various corporate purposes, such as funding growth initiatives or reducing debt. Common stock, on the other hand, represents the basic form of equity capital that is available to the company for financing its operations.

In conclusion, while both APIC and common stock are essential components of a company’s financial structure, they differ in terms of their sources, accounting treatment, impact on financial statements, and roles in the capital structure. Understanding these differences can help investors and financial analysts better assess the financial health and performance of a company.

Steps to record APIC in a company’s financial statements

Additional Paid-In Capital (APIC) is a term used in accounting that refers to the excess amount of money a company receives from investors above the par value of its stock. It is recorded on the balance sheet as part of shareholders’ equity. Here are the steps to properly record APIC in a company’s financial statements:

1. Determine the amount of APIC: Before recording APIC in the financial statements, the company needs to calculate the excess amount of money received from investors above the par value of the stock. This can be done by subtracting the par value of the stock from the total amount received from investors.

2. Create a separate APIC account: In order to accurately track APIC, it is important to set up a separate account on the balance sheet specifically for recording this type of capital. This helps in distinguishing APIC from other components of shareholders’ equity.

3. Record the initial APIC entry: Once the amount of APIC has been determined and a separate account has been created, the company should record the initial entry for APIC. This involves debiting cash or another asset account for the total amount received from investors and crediting the APIC account for the excess amount above the par value.

4. Adjust for any changes in APIC: Over time, the amount of APIC may change due to additional investments, stock repurchases, or other transactions. It is important for the company to regularly review and adjust the APIC account to reflect any changes in the amount of excess capital received from investors.

5. Disclose APIC in the financial statements: In addition to recording APIC on the balance sheet, the company should also disclose the amount of APIC in the notes to the financial statements. This helps provide transparency to investors and other stakeholders about the company’s capital structure and the amount of excess capital received from investors.

Overall, recording APIC in a company’s financial statements involves accurately calculating the excess amount of money received from investors, creating a separate account for APIC, recording the initial entry, adjusting for any changes, and disclosing the amount of APIC in the financial statements. By following these steps, companies can ensure that their financial statements accurately reflect the amount of excess capital received from investors above the par value of the stock.

Originally posted 2025-02-12 06:50:02.